Navigating the 2024 tax landscape requires diligent preparation and awareness of crucial deadlines; expert guidance is readily available to assist filers.

Welcome to the 2024 tax season! As we approach the filing deadline‚ understanding the nuances of this year’s tax regulations is paramount. Tax season is upon us‚ with a crucial window for completion closing around mid-April. Remember‚ your 2024 tax return reflects financial activity from the previous year‚ demanding careful review of all relevant documentation.

This guide serves as a comprehensive resource‚ offering insights into key dates‚ filing procedures‚ and essential tax concepts. The Canadian Revenue Agency (CRA) has recently updated Schedule 3‚ focusing on Capital Gains or Losses‚ highlighting the importance of staying current with form revisions. Given economic uncertainties‚ proactive tax planning is especially beneficial for business owners seeking to optimize their financial strategies.

Retirement also significantly impacts your tax obligations‚ necessitating a clear understanding of how benefits and distributions are taxed.

Key Dates and Deadlines for 2024 Filing

Mark your calendars! The primary deadline for filing your 2024 taxes is April 15th. This date is critical for individuals to submit their returns and avoid potential penalties. With approximately two weeks remaining as of mid-April 2026‚ timely action is crucial. Remember‚ this deadline applies to the vast majority of taxpayers‚ covering income and financial events from the 2024 calendar year.

However‚ it’s important to note that extensions may be available under certain circumstances. Taxpayers should investigate eligibility for extensions if they anticipate difficulties meeting the standard April 15th deadline. Staying organized and gathering necessary paperwork now will streamline the filing process and ensure compliance. Don’t delay – proactive preparation is key to a stress-free tax season!

Keep an eye out for any official announcements from the CRA regarding potential adjustments to these dates.

General Filing Information

Understanding the basics is paramount. Filing your 2024 taxes primarily revolves around events that transpired throughout last year – the 2024 calendar year. Gathering all relevant financial documentation‚ including income statements (W-2s‚ 1099s) and records of deductible expenses‚ is the first crucial step. Most taxpayers will utilize Form 1040‚ the U.S. Individual Income Tax Return‚ as the foundation for their filing.

Remember that nearly everything impacting your return occurred in 2024‚ necessitating a thorough review of that year’s financial activity. Whether filing independently or utilizing tax preparation software‚ accuracy and completeness are vital. Consider seeking professional assistance if your tax situation is complex or if you’re unsure about specific deductions or credits.

Staying informed about changes to tax laws and regulations is also highly recommended.

Income Tax Basics

Income tax fundamentals involve understanding brackets‚ deductions‚ and income classifications; these elements determine your tax liability for the 2024 filing year.

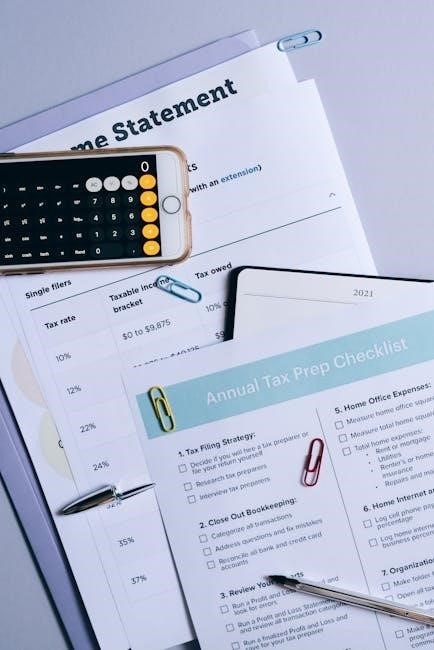

Tax Brackets for 2024

Understanding the 2024 tax brackets is crucial for calculating your income tax liability. These brackets define the percentage of income taxed at each level. For single filers‚ the brackets typically range from 10% to 37%‚ with thresholds increasing with income. Married filing jointly have different‚ generally higher‚ thresholds.

The 2024 brackets determine how much of your income falls into each tax rate. For example‚ income up to a certain amount might be taxed at 10%‚ while income exceeding that amount is taxed at a higher rate. It’s important to note that these are marginal rates – only the portion of income within each bracket is taxed at that rate. Knowing these brackets allows for accurate tax planning and potential strategies to minimize your overall tax burden. Consult official IRS resources for precise bracket amounts.

Standard Deduction and Itemized Deductions

Taxpayers filing in 2024 have a choice: taking the standard deduction or itemizing deductions. The standard deduction is a fixed amount that reduces your taxable income‚ simplifying the tax process. Its amount varies based on filing status – single‚ married filing jointly‚ etc. – and is adjusted annually for inflation.

Itemized deductions‚ however‚ allow you to list specific expenses – like medical expenses‚ state and local taxes (SALT)‚ and mortgage interest – to potentially lower your tax liability further. Choosing between the standard deduction and itemizing depends on whether your itemized deductions exceed the standard deduction amount. Carefully calculating both options is essential to maximize your tax savings and ensure accurate filing for the 2024 tax year.

Taxable vs. Non-Taxable Income

Understanding which types of income are taxable and which are not is fundamental to accurate tax filing in 2024. Generally‚ most income you receive – wages‚ salaries‚ tips‚ and business income – is considered taxable and must be reported to the IRS. However‚ certain types of income are specifically excluded from taxation.

Examples of potentially non-taxable income include gifts‚ inheritances‚ and certain types of insurance benefits. Additionally‚ some employee benefits may be partially or fully tax-free. It’s crucial to differentiate between these income sources to avoid errors on your tax return. Proper categorization ensures you only pay taxes on income legally required‚ optimizing your financial outcome during this tax season.

Common Tax Credits and Deductions

Numerous credits and deductions‚ like the Child Tax Credit and Earned Income Tax Credit‚ can significantly reduce your 2024 tax liability; explore eligibility.

Child Tax Credit

The Child Tax Credit is a valuable benefit for eligible taxpayers with qualifying children. For the 2024 tax year‚ the maximum credit amount is generally $2‚000 per qualifying child. A qualifying child must meet specific requirements regarding age‚ relationship‚ residency‚ and support. Importantly‚ a portion of the credit may be refundable‚ meaning you could receive some of it back even if you don’t owe any taxes.

The refundable portion‚ known as the Additional Child Tax Credit‚ can be up to $1‚600 per child. Income limitations apply‚ and the credit phases out for higher-income taxpayers. To claim the Child Tax Credit‚ you must file Form 1040 and attach Schedule 8812‚ Credits for Qualifying Children and Other Dependents. Careful attention to the eligibility rules and proper documentation is crucial for a successful claim.

Earned Income Tax Credit

The Earned Income Tax Credit (EITC) is a refundable tax credit designed to assist low-to-moderate income workers and families. For 2024‚ the maximum credit amount varies depending on your filing status and the number of qualifying children. Eligibility is determined by adjusted gross income (AGI) and earned income‚ with specific limits that change annually.

To qualify‚ you generally must have earned income‚ meet certain residency requirements‚ and have a valid Social Security number. The EITC can significantly reduce your tax liability and even provide a refund‚ even if you owe no taxes. Claiming the EITC requires filing Form 1040 and completing Schedule EIC‚ Earned Income Credit. Accurate reporting of income and qualifying child information is essential for a successful claim.

Education Credits (Lifetime Learning Credit‚ American Opportunity Credit)

Taxpayers pursuing higher education‚ or those with qualifying students‚ may be eligible for valuable education tax credits. The American Opportunity Credit (AOC) is for the first four years of higher education‚ offering a maximum credit of $2‚500 per student. It’s partially refundable‚ meaning you might get some back even if you owe no taxes.

The Lifetime Learning Credit (LLC) is available for all years of higher education and for courses taken to acquire job skills. It provides a credit of up to $2‚000 per tax return‚ not per student. Eligibility depends on income limits and enrollment in eligible educational institutions. Claiming these credits requires Form 8863‚ Education Credits‚ filed with your Form 1040.

Retirement Savings Contributions Credit (Saver’s Credit)

The Saver’s Credit‚ also known as the Retirement Savings Contributions Credit‚ assists low-to-moderate income taxpayers in saving for retirement. This nonrefundable credit can reduce your tax liability based on contributions made to a qualified retirement plan‚ such as a 401(k) or IRA.

The maximum credit is $1‚000 for single filers and $2‚000 for those married filing jointly. Credit percentages vary based on adjusted gross income (AGI)‚ decreasing as income rises. To qualify‚ you must be at least 18‚ not a full-time student‚ and have earned income. Form 8880‚ Credit for Qualified Retirement Contributions‚ is used to claim this credit when filing your federal income tax return.

Capital Gains and Losses

Understanding the distinction between short-term and long-term capital gains is vital for accurate tax reporting‚ especially with updated Schedule 3 forms.

Short-Term vs. Long-Term Capital Gains

Capital gains arise when you sell an asset for more than you purchased it for‚ and how long you held the asset dictates the tax treatment. Short-term capital gains apply to assets held for one year or less‚ taxed at your ordinary income tax rate – meaning they’re taxed the same as your wages or salary.

Conversely‚ long-term capital gains are realized from assets held for over one year‚ and generally benefit from lower tax rates than ordinary income. These rates are typically 0%‚ 15%‚ or 20%‚ depending on your taxable income. Understanding this distinction is crucial‚ as it significantly impacts your overall tax liability. Careful tracking of purchase dates and sale proceeds is essential for accurate reporting on Schedule D.

The updated 2024 Schedule 3 from the CRA highlights the importance of correctly classifying these gains to ensure compliance and potentially minimize your tax burden.

Reporting Capital Gains on Schedule D

Schedule D (Form 1040)‚ Capital Gains and Losses‚ is the key form for reporting the profit or loss from selling capital assets like stocks‚ bonds‚ and real estate. This form requires detailed information about each transaction‚ including the date acquired‚ date sold‚ sales price‚ and your cost basis (original purchase price plus any improvements).

Accurately completing Schedule D is vital‚ as it directly impacts your taxable income. You’ll calculate your overall capital gain or loss‚ which then transfers to Form 1040. The recent update to the CRA’s 2024 Schedule 3 emphasizes the need for precise record-keeping to support your reported figures.

Remember to differentiate between short-term and long-term gains‚ as they are reported separately on the form and taxed at different rates.

Capital Losses and Their Limitations

Capital losses arise when you sell a capital asset for less than your cost basis. While these losses can offset capital gains‚ the IRS imposes limitations on their deductibility. You can use capital losses to offset capital gains of the same type – short-term losses offset short-term gains‚ and long-term losses offset long-term gains.

If your capital losses exceed your capital gains‚ you can deduct up to $3‚000 ($1‚500 if married filing separately) of the excess loss from your ordinary income each year. Any remaining loss can be carried forward to future tax years.

Accurate reporting on Schedule D is crucial for claiming these deductions.

Self-Employment Taxes

Self-employed individuals face unique tax obligations‚ including self-employment tax‚ which covers Social Security and Medicare; strategic planning is essential.

Self-Employment Tax Rate

Understanding the self-employment tax rate is crucial for freelancers‚ contractors‚ and business owners. This tax essentially covers both the employer and employee portions of Social Security and Medicare taxes. For 2024‚ the self-employment tax rate remains at 15.3%. This breaks down to a 12.4% Social Security tax on the first $168‚600 of net earnings (as of 2024) and a 2.9% Medicare tax on all net earnings.

However‚ you don’t pay self-employment tax on the entire amount of your net profit. You first get to deduct one-half of your self-employment tax from your gross income. This adjustment to income helps to level the playing field with traditional employees‚ who don’t pay both sides of these taxes. Careful calculation and accurate reporting are vital to avoid potential issues with the IRS.

Deductions for Self-Employment Tax

Self-employed individuals benefit from several key deductions that can significantly reduce their tax liability. The most prominent is the deduction for one-half of self-employment tax. This means you can subtract half the amount of Social Security and Medicare taxes paid from your gross income‚ lowering your adjusted gross income (AGI). This deduction is claimed on Schedule 1 (Form 1040).

Beyond this‚ standard business expenses are fully deductible‚ including costs for office supplies‚ equipment‚ travel‚ and professional development. Maintaining meticulous records of all expenses is paramount. Furthermore‚ the Qualified Business Income (QBI) deduction‚ potentially allowing a deduction of up to 20% of QBI‚ can offer substantial savings‚ subject to certain income limitations and rules. Proper planning and documentation are essential to maximize these benefits.

Estimated Tax Payments

Self-employed individuals‚ freelancers‚ and those with income not subject to withholding typically need to make estimated tax payments throughout the year. These payments‚ made quarterly‚ cover income tax and self-employment tax obligations. Failing to pay enough estimated tax can result in penalties‚ so accurate calculation is crucial.

The IRS generally requires estimated tax payments if you expect to owe at least $1‚000 in taxes. Payment due dates usually fall on April 15‚ June 15‚ September 15‚ and January 15 of the following year. Utilizing Form 1040-ES facilitates these payments. Several methods are available‚ including online‚ by mail‚ or through the Electronic Federal Tax Payment System (EFTPS). Careful income projection and consistent monitoring are vital for avoiding underpayment penalties.

Retirement Income and Taxes

Retirement marks a significant tax shift; understanding how Social Security‚ IRAs‚ and 401(k) distributions are taxed is essential for effective financial planning.

Taxation of Social Security Benefits

Determining the taxability of Social Security benefits can be complex‚ depending on your overall income. Up to 85% of your Social Security benefits may be subject to federal income tax‚ but this depends on your “combined income.” Combined income is calculated by adding your adjusted gross income (AGI)‚ nontaxable interest‚ and one-half of your Social Security benefits.

If your combined income exceeds certain thresholds – $25‚000 for single filers‚ $32‚000 for married filing jointly‚ and $0 for married filing separately – then a portion of your benefits will be taxable. These thresholds are subject to change annually. Understanding these rules is crucial for accurate tax filing‚ especially as retirement income streams become more significant. Careful planning can help minimize the tax impact on these essential benefits.

Distributions from Traditional IRAs and 401(k)s

Distributions from traditional IRAs and 401(k)s are generally taxed as ordinary income in the year they are taken. This is because contributions to these accounts were often made with pre-tax dollars‚ offering a tax deduction at the time of contribution. Consequently‚ when funds are withdrawn in retirement‚ they are taxed at your current income tax rate.

However‚ there are exceptions and potential penalties for early withdrawals (before age 59 ½)‚ unless certain qualifying events occur. Required Minimum Distributions (RMDs) also begin at a specific age‚ forcing withdrawals and subsequent taxation. Careful planning regarding withdrawal strategies is essential to manage your tax liability and maximize your retirement income.

Roth IRA Withdrawals

Qualified withdrawals from a Roth IRA are generally tax-free and penalty-free. This is a significant benefit‚ as contributions are made with after-tax dollars‚ meaning you’ve already paid taxes on the money. To be considered “qualified‚” the withdrawal must occur after age 59 ½ and the account must be open for at least five years.

However‚ withdrawals of earnings before meeting these requirements may be subject to both income tax and a 10% penalty. Contributions‚ on the other hand‚ can always be withdrawn tax-free and penalty-free. Understanding these rules is crucial for maximizing the benefits of a Roth IRA during retirement and avoiding unexpected tax consequences.

Important Forms and Schedules

Accurate tax filing relies on utilizing the correct forms‚ including 1040‚ Schedule 1‚ Schedule 3 for capital gains‚ and Schedule SE for self-employment tax;

Form 1040 ‒ U.S. Individual Income Tax Return

Form 1040 is the cornerstone of the U.S. federal income tax system‚ serving as the primary document for individuals to report their annual income‚ deductions‚ and credits. For the 2024 tax year‚ this form remains central to the filing process‚ requiring taxpayers to meticulously detail all sources of income‚ including wages‚ salaries‚ interest‚ dividends‚ and any other taxable earnings.

The form’s structure guides filers through calculating their adjusted gross income (AGI) by subtracting eligible deductions from their total income. Subsequently‚ taxpayers determine their taxable income by choosing between the standard deduction or itemizing deductions‚ such as medical expenses‚ state and local taxes‚ and mortgage interest.

Finally‚ Form 1040 facilitates the calculation of tax liability based on the applicable tax brackets and allows for the application of tax credits to reduce the overall tax owed. Accurate completion of this form is paramount for ensuring compliance with IRS regulations and avoiding potential penalties.

Schedule 1 ⎼ Additional Income and Adjustments to Income

Schedule 1 of Form 1040 is crucial for reporting income sources beyond typical wages and salaries‚ and for detailing adjustments to income that reduce your taxable amount. This form accommodates various income types‚ including business income‚ capital gains‚ rental real estate‚ royalties‚ and unemployment compensation.

Adjustments to income‚ often referred to as “above-the-line” deductions‚ are reported here and directly lower your AGI. Common adjustments include contributions to traditional IRAs‚ student loan interest payments‚ health savings account (HSA) deductions‚ and alimony paid (for divorce agreements finalized before 2019).

Accurately completing Schedule 1 ensures a comprehensive and correct calculation of your AGI‚ impacting your overall tax liability. It’s essential to gather all relevant documentation for both additional income and adjustments to maximize potential tax savings.

Schedule 3 ‒ Capital Gains (Losses)

Schedule D (Capital Gains and Losses)‚ often accessed through Schedule 3‚ is where you report profits from the sale of capital assets like stocks‚ bonds‚ and real estate. Understanding the distinction between short-term (held for a year or less) and long-term capital gains is vital‚ as they are taxed at different rates.

This schedule requires detailed record-keeping of purchase prices‚ sale proceeds‚ and any related expenses. Capital losses can offset capital gains‚ and any excess losses can be deducted against ordinary income‚ subject to limitations – currently capped at $3‚000 per year.

The recent update to the CRA’s 2024 Schedule 3 highlights its importance. Accurate reporting on this form is crucial for minimizing tax liability and ensuring compliance with tax regulations.

Schedule SE ⎼ Self-Employment Tax

Schedule SE is pivotal for individuals earning income as independent contractors‚ freelancers‚ or business owners. It calculates the self-employment tax‚ which encompasses both Social Security and Medicare taxes – typically shared between employer and employee‚ but fully borne by the self-employed.

The current self-employment tax rate is 15.3% (12.4% for Social Security up to the wage base limit‚ and 2.9% for Medicare). However‚ you can deduct one-half of your self-employment tax from your gross income‚ reducing your adjusted gross income (AGI).

Effective tax planning for self-employment involves maximizing eligible deductions to minimize this tax burden. Accurate completion of Schedule SE is essential for proper tax calculation and avoiding potential penalties.